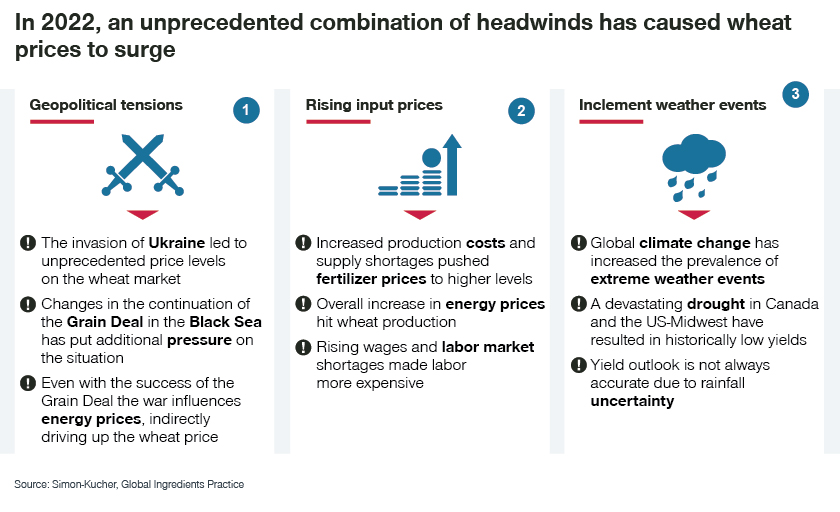

An unfortunate series of events has led to historically high prices for wheat. The combination of geopolitics, impacting both the supply of wheat and its inputs, as well as increasing occurrences of extreme weather, have created the perfect storm. These headwinds are not likely to weaken in 2023. As a consequence, wheat prices likely will remain high in the coming months.

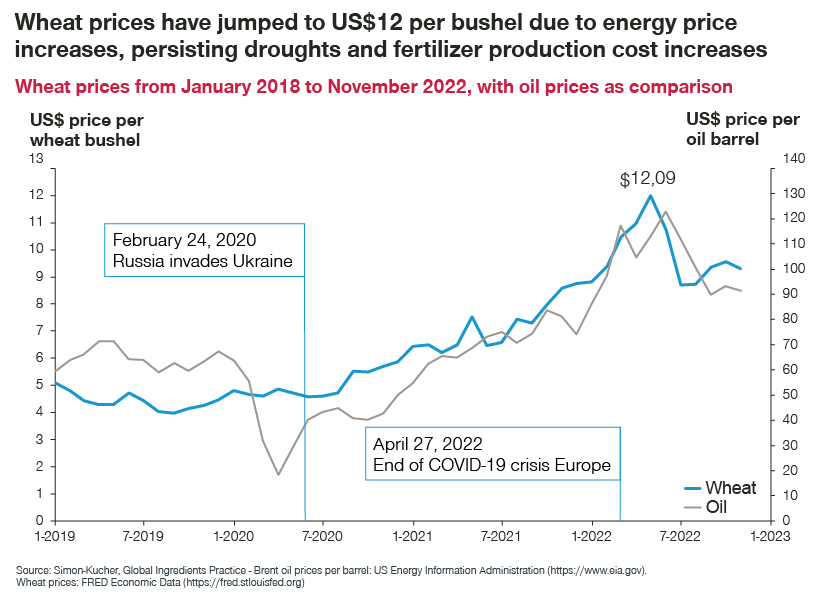

In March 2022, wheat prices rose to an unprecedented price level of more than 12 US dollars per bushel (Trading Economics, 2022). The re-emergence of war in Europe had given rise to uncertainty within many supply chains, food and agriculture included. Suddenly, 28 percent of worldwide wheat exports were at risk (FAO, 2022). This potential drop in supply constituted a major challenge to a wheat supply chain that was already under stress. Rising fuel and fertilizer prices and a major drought in the northern hemisphere, resulting in unexpectedly low harvest yields, caused further upward pressure on wheat prices.

These headwinds have somewhat weakened. The extended Black Sea deal between Russia and Ukraine has provided some certainty on the export of wheat. Rainfall has also been more at historical norms than in 2021. However, both the war and rainfall are hard to predict, certainly over longer periods of time. This, combined with an already existing shortage of wheat, makes it unlikely that prices will decrease soon.

Input costs remain at historic highs

The last year has seen steep price increases for several input factors of wheat production. The most significant component, fertilizer, is a striking example. Prices had been steady between 2018 and 2021, but almost tripled in 2022 (YCharts, 2022). The geopolitical crisis in Ukraine is a root cause, with two impact levers.

First, the price of energy, particularly in Europe, has directly been impacted by the war, resulting in more costly production of energy-intensive chemical products like fertilizer. Second, Ukraine, Russia, and Belarus together account for over 40 percent of global fertilizer supply (CNBC, 2022). The war has directly caused a large part of the global fertilizer supply to be unreachable. With these circumstances expected to remain in the coming months, fertilizer prices are expected to rise even further.

Direct energy usage in the production of crops has also increased with the increasing mechanization and automation of large-scale agriculture. Since wheat production is highly energy intensive in developed economies, the price increases are directly transferred into the value chain (IEA, 2022). The 2023 outlook for energy prices is better than for fertilizer, but a decrease in price is only likely in the more optimistic scenarios. A final, and proportionally smaller cost component to consider, is manual labor costs which have also increased sharply and are expected to rise even more due to labor market shortages.

Regional yields have been unevenly impacted by rainfall this year

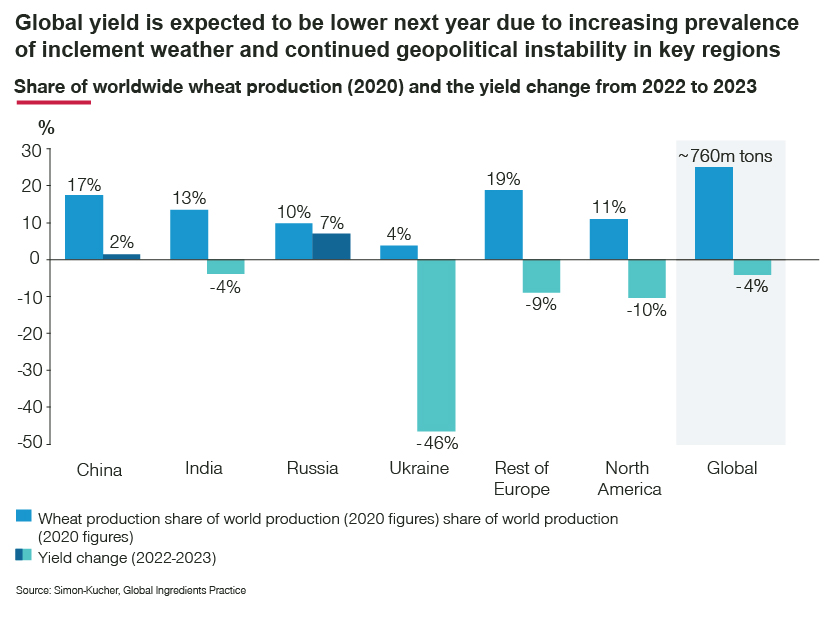

The gradual pace of global climate change has a fundamental impact on wheat yields. In the longer term, climate change could force a shift in location where weather conditions are optimal for growing wheat (NASA, 2021). A consequence of climate change is the increased prevalence of drought. This has had a short-term impact on wheat yields. For example, a devastating drought in the Canadian prairies caused wheat yields to be approximately 27 percent lower in 2021 than the average over the past ten years (Index Mundi, 2022). The extreme impact of drought on crop yield volatility will continue into the 2022-2023 period where with nominal amounts of rainfall in H2’2023 are expected to realize yields about 14 percent higher than the ten-year average.

The outlook for the United States (US) and European Union (EU) is less optimistic. While yields in the US are expected to be similar to this year, the EU harvest is expected to worsen by about three percent (USDA, 2022). The wheat market’s dynamics mitigate sharp supply spikes across global prices and consequently, the large, expected increase of supply in Canada will have the largest impact directly on the prices in North America which will have net-positive yield versus the previous year (WUR, 2022). The supply increase is expected to have a smaller impact on global prices in 2023 and we forecast this will drive down prices by around three percent.

Geopolitical tensions continue to stress the market

The invasion of Ukraine severely disrupted the wheat market. Wheat prices surged to unprecedented levels and immediate concerns about food shortages were raised (Trading Economics, 2022). This impact is not surprising, since Russia and Ukraine combined are responsible for around 28 percent of global wheat exports (FAO, 2022). After this initial spike of uncertainty, the market somewhat calmed down. But, only from the end of June, when Ukraine and Russia started talking about a potential Black Sea grain deal, did prices decrease more steeply (Trading Economics, 2022). Ultimately, a price level consistent with pre-war prices was reached.

The conflict, however, continues to have a large impact on global wheat prices. When Russia announced that it would pull out of the Black Sea deal, wheat prices jumped by about seven percent. After Russia rejoined the deal several days later, prices decreased again, by the same amount they had gone up. This displays the pressure that geopolitical tensions in general, and the war between Russia and Ukraine in particular, can have on the wheat market. A continuously changing situation in Eastern Europe could drive prices up even more in 2023. Unfavorable developments have the potential to push prices up by about five percent.

The headwinds are unlikely to weaken in 2023. Rising fertilizer and energy prices, the unpredictability of rain, and the tense situation in Eastern Europe are all driving up wheat prices. In this perfect storm of circumstances, wheat prices are expected to remain well above the 300 USD/MT level in 2023, with a high likelihood of reaching the 340 USD/MT range during the summer.

How the food ingredients industry is adapting to the new norm

Commercial agility has been the keyword throughout the current geopolitical situation. While the pandemic forced many companies across all industries to become leaner, the post-pandemic world places commercial levers front-and-center as cost-cutting levers have largely been expended.

Digital capability has long been accepted as a crucial agility lever. One less popular, but no less important, is that of an adaptable organization.

In a best practice example, one of our clients undertook an organizational redesign to take procurement away from the COO and place it under the reporting line of the CCO. This immediately resulted in increased connectivity between pricing, sales, and procurement. Customers were presented with more accurate and up-to-date prices, even against unprecedented inflation. Another benefit was the increased visibility procurement had on commercial priorities, enabling them to prioritize supplier contract negotiations and consequently fight harder for the products sales and pricing strategically cared about. Our client was able to finish 2022 with strong growth while their closest peers and overall market segment were stagnant.

Further insights into how to improve your price increase success rate can be found here. For more research into commodity prices or how you can better prepare your organization for upcoming economic uncertainty, don’t hesitate to reach out – we’re here to help.